New Listings and Pending Sales

Heartland Real Estate Professionals

Jean Youness 651-336-5042

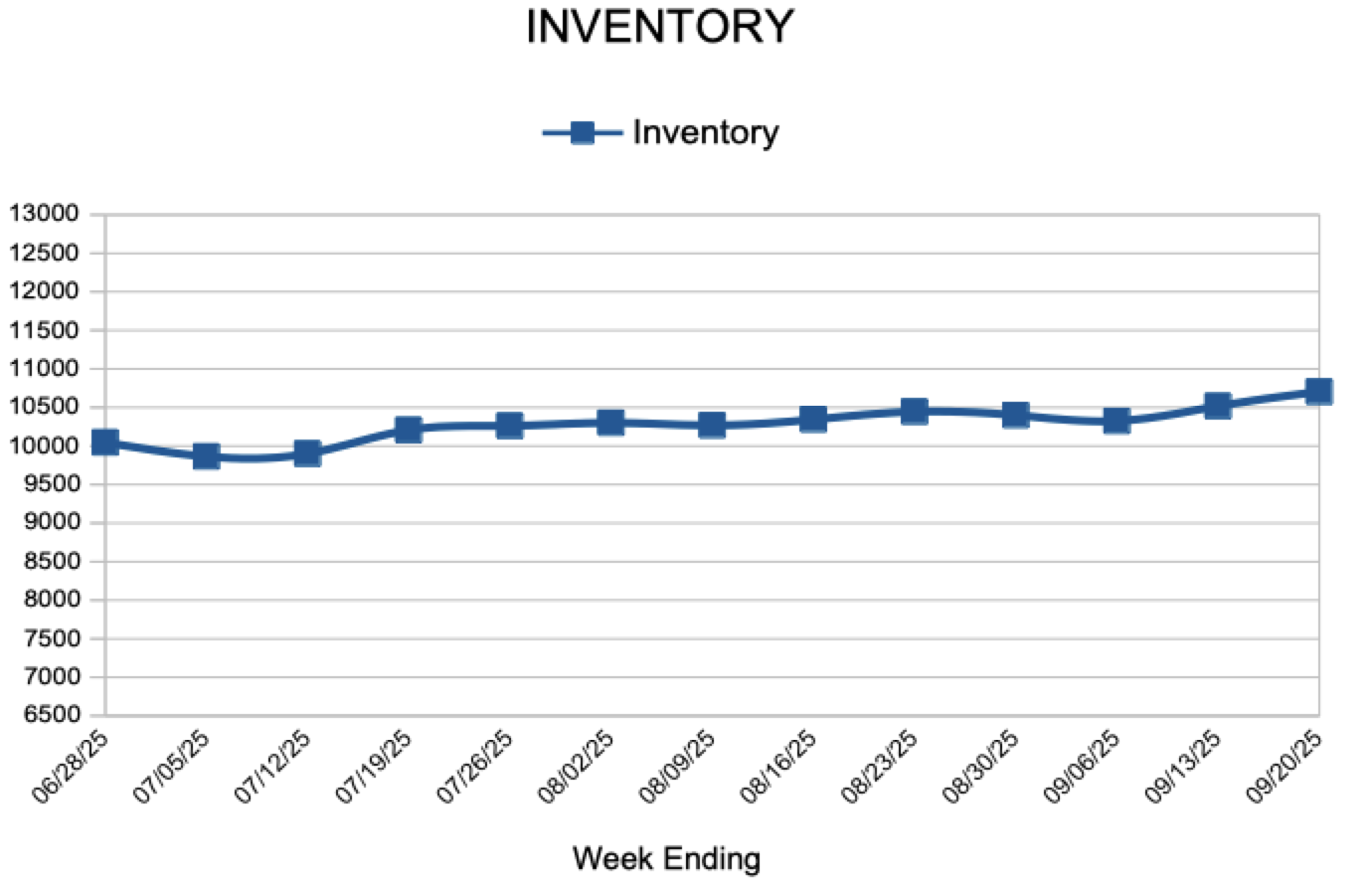

For Week Ending October 4, 2025

For Week Ending October 4, 2025

Nationally, the best time to buy a home is the week of October 12–18, according to a recent report from Realtor®.com. Historically, this week offers the most favorable conditions for buyers, with higher inventory levels, lower home prices, reduced competition, and a slower market pace. However, the optimal buying window varies across local markets. Some areas have already experienced peak buyer conditions, while others may not reach their ideal period until November or December.

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING OCTOBER 4:

FOR THE MONTH OF AUGUST:

All comparisons are to 2024

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.

October 9, 2025

Mortgage rates decreased this week. Over the last few weeks, mortgage rates have settled in at their lowest level in about a year. There is growing evidence that homebuyers are digesting these lower rates and gradually are willing to move forward with buying a home, which is boosting purchase activity.

Information provided by Freddie Mac.

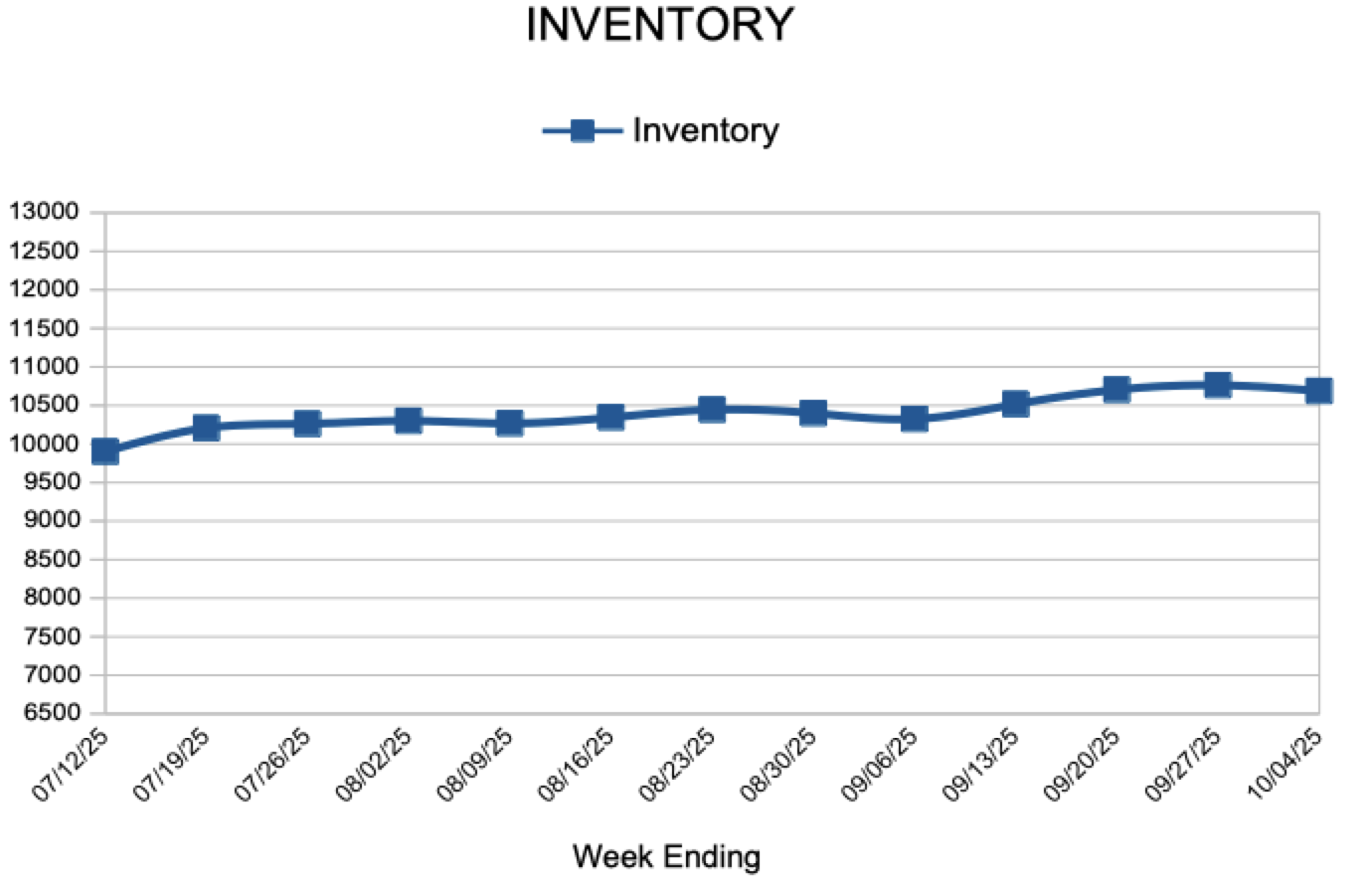

For Week Ending September 27, 2025

For Week Ending September 27, 2025

According to ATTOM’s Q2 2025 Home Equity and Underwater Report, 47.4% of mortgaged residential properties in the U.S. were considered equity-rich—defined as having at least 50% equity—in the second quarter of 2025. This marks an improvement from the first quarter, when 46.2% of mortgaged homes met that threshold, ending a trend of three consecutive quarterly declines.

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING SEPTEMBER 27:

FOR THE MONTH OF AUGUST:

All comparisons are to 2024

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.

October 2, 2025

The 30-year fixed-rate mortgage increased again this week but remains below its 52-week average of 6.71%. The last few months have brought lower rates and as indicated by the recently reported increase in pending home sales, homebuyers are feeling more confident to get into the market.

Information provided by Freddie Mac.